Enterprise AI Moat.

Why incumbents with embedded distribution are pulling ahead over a 10 to 15 year cycle.

CMI Market Intelligence | Insights

January 24, 2026

A close reading of recent market commentary highlights a practical point that is easy to miss amid the headlines. Enterprise AI adoption will be driven less by new, standalone AI vendors and more by incumbent workflow software providers that already own distribution, data adjacency, and trust inside regulated organizations. The investment implication is narrower than the hype, but potentially durable for the right franchises.

Enterprise AI is most likely to be commercialized by workflow incumbents with deep domain embed, not by generic AI tooling.

AI value in the enterprise will skew toward productivity and workflow compression, not wholesale labor replacement.

Valuation compression in software has reopened strategic consolidation pathways, but integration risk remains the gating factor.

Private equity can accelerate outcomes by professionalizing operations and positioning assets for strategic absorption.

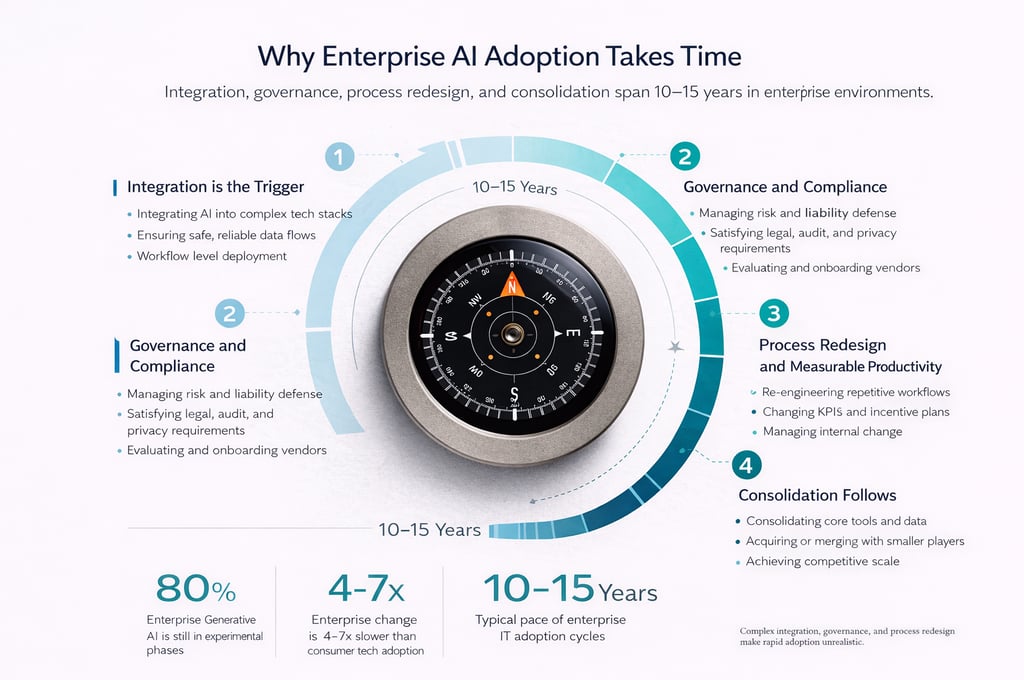

The adoption curve is measured in years, not quarters. Expect an evolutionary transition that rewards patient execution.

Key Insights

The enterprise reality. AI moves at the speed of governance

Public discussion around AI often assumes an abrupt shift in enterprise operating models. In practice, large organizations change slowly because systems are interconnected, data is messy, and risk is asymmetric. Every new capability must clear procurement, security review, data access controls, audit requirements, and, in many sectors, regulatory scrutiny. The result is an adoption curve that is typically evolutionary rather than revolutionary.

This framing matters because it sets the right expectations for investors and operators. If enterprise AI is a multi-year transition, near-term volatility in sentiment and valuation is not the same thing as structural impairment. Conversely, early pilots are not proof of durable monetization. The focus should be on how value is captured in production, at scale, within the constraints of the enterprise environment.

Why incumbents are positioned to win

The most credible path to enterprise AI adoption runs through existing workflow platforms. Enterprises rarely deploy AI as a standalone tool. They deploy it where it reduces friction in systems already used daily, where permissions are known, where data is proximate, and where output can be audited. This is why domain-centric software companies, particularly those embedded in industrial and regulated workflows, are central to the next phase.

The differentiator is not simply model quality. It is domain franchise. In workflow software, domain franchise means deeply encoded process knowledge, integration surface area, and trust capital with users and IT teams. These assets are built over long periods and are difficult to replicate quickly by newcomers. AI can enhance the product, but it cannot instantly recreate the decade of implementations, edge cases, controls, and customer-specific configurations that make mission-critical software sticky.

In practical terms, AI value tends to come from compressing handoffs and automating routine judgment inside an existing process. That implies productivity gains for the labor already operating within the system. The most investable outcomes are the measurable ones: fewer touches, fewer errors, faster cycle times, and higher throughput using the same underlying workflow architecture.

The valuation reset is creating selective opportunity

Software valuations have repriced materially from the peak of the prior cycle. Some of this adjustment reflects higher discount rates. Some reflects uncertainty over how AI will alter competitive dynamics and pricing power. The key is to distinguish between companies experiencing multiple compression because of macro conditions and companies facing genuine moat erosion.

For high-quality workflow incumbents, a lower multiple does not necessarily indicate weakened fundamentals. If the platform remains embedded, retention remains strong, and AI features improve outcomes without destabilizing gross margins, the repricing may create entry points. The discipline is to underwrite cash flow durability and reinvestment needs, not to buy the dip broadly.

M&A returns as a primary strategy, with AI as a catalyst

A second-order effect of the valuation reset is renewed appetite for consolidation. Large software vendors can often acquire smaller capabilities at prices that are more rational than they were several years ago. In that context, AI functions less as the core rationale and more as a catalyst. AI increases the value of owning adjacent data, reducing workflow fragmentation, and offering end-to-end outcomes rather than point features.

The strongest acquirers are those with distribution and workflow control. They can integrate adjacent products, cross-sell into an installed base, and rationalize overlapping research and development and general and administrative cost. However, consolidation is not automatically value-creating. The gating factor is integration execution: product overlap decisions, roadmap clarity, customer migration, and retention of key technical talent.

Acquirers are rewarded when a deal deepens platform control, improves net retention, and preserves margin structure. They are penalized when acquisitions appear defensive, margin-dilutive, or distracting. In this cycle, the market is more skeptical of empire-building and more sensitive to integration risk than it was in the prior expansion.

Where private equity fits, and what it can realistically change

Private equity is structurally aligned with this transition because the work is operational, not theoretical. Many domain software companies have strong products but uneven execution: under-optimized pricing, bloated go-to-market spend, under-invested customer success, and limited discipline in product scope. Professionalizing operations and tightening focus can create strategic assets that are easier for platform acquirers to absorb.

Claims of expanding operating margins from roughly 10 percent to 40 percent should be treated as an execution plan, not a slogan. It is achievable in certain business models when gross margins are strong and retention is durable, but it requires tradeoffs: simplifying the product, improving implementation, reducing non-core complexity, and aligning incentive systems to long-term retention. Margin expansion that starves product investment or customer support can backfire by increasing churn and weakening the franchise.

The time horizon mismatch. Why this is a 10 to 15 year story, possibly longer

Estimates of 10 to 15 years for meaningful enterprise transformation are plausible, and in some industries may be conservative. Enterprises adopt technology slowly because they optimize for uptime, compliance, and continuity. AI will be incorporated where it is provably safe, auditable, and economically rational, and that proof often comes only after repeated deployments.

For operators, this argues for disciplined productization and patient rollout. For investors, it argues for underwriting durable franchises and balance sheet resilience rather than short-term narrative. The likely winners are the companies that translate AI into tangible workflow outcomes while preserving trust and economics over a long horizon.

Evidence of monetization. AI features tied to pricing, usage expansion, or measurable net retention improvement.

Cost structure. Gross margin impact after compute and model costs, and whether unit economics remain attractive at scale.

Implementation cycle. Time-to-value, security approvals, and the extent to which procurement friction slows deployments.

Consolidation quality. Clear post-merger product roadmaps, measured customer migration, and retention of key talent.

What to Watch

Enterprise AI is likely to be a long transition that favors incumbents with domain franchise and disciplined execution. The opportunity is meaningful, but it will accrue to a narrower set of companies than the broad AI narrative suggests. Operational proof will separate durable winners from transient excitement.

© 2025 CurveMind Inc. All rights reserved. CMI Market Intelligence is a division of CurveMind Inc.