Rate Cuts With a Catch

Warsh at the Fed? Rate Cuts With a Catch for Real Estate and Equity Markets

Thesis

The central question is whether rate cuts would pull down the whole curve. If short rates fall but term premiums stay high, real estate does not get meaningful relief, and equity upside is mostly sentiment-driven.

A Warsh playbook that pairs faster policy rate cuts with balance-sheet shrinkage is not a pure easing. It is a rebalancing of levers. Cuts loosen the front end. QT can keep pressure on duration, MBS spreads, and risk premia.

Real estate is effectively a leveraged long-duration asset. The magnitude of the move in mortgage rates and cap rates, not Fed funds, will determine transaction volume and valuation stabilization.

Equities can rally on the headline, but durable multiple expansion requires lower real long rates and a stable equity risk premium. If investors perceive compromised Fed independence or fiscal dominance, the long end can reprice higher and negate the stimulus.

CMI Market Intelligence | Insights

February 1, 2026

What Hassett signaled in the interview excerpt

In a CNBC “Squawk on the Street” interview on January 30, 2026, National Economic Council Director Kevin Hassett endorsed President Trump’s nomination of Kevin Warsh to lead the Federal Reserve and emphasized urgency in securing a swift confirmation.

Hassett’s market-relevant message had three parts. First, he framed the current expansion as supply-driven, analogous to the late-1990s productivity cycle, implying higher potential growth without persistent inflation.

Second, he argued that fiscal restraint and deficit reduction should ease Treasury financing pressure over time and help bring yields down across maturities.

Third, he reiterated the administration’s view that policy is currently too tight, while stopping short of speaking for Warsh’s specific settings.

The signaling is consistent with a White House preference for easier financial conditions, paired with a narrative of disinflation and improved fiscal posture, as the nomination moves through a confirmation process that is already entangled with political scrutiny of the Fed’s headquarters renovation project.

The Warsh setup. Cuts plus balance-sheet discipline

Reporting on the nomination describes Warsh as critical of an oversized Fed balance sheet and open to lower rates, but with the important qualifier that rate cuts are more credible when paired with balance-sheet shrinkage.

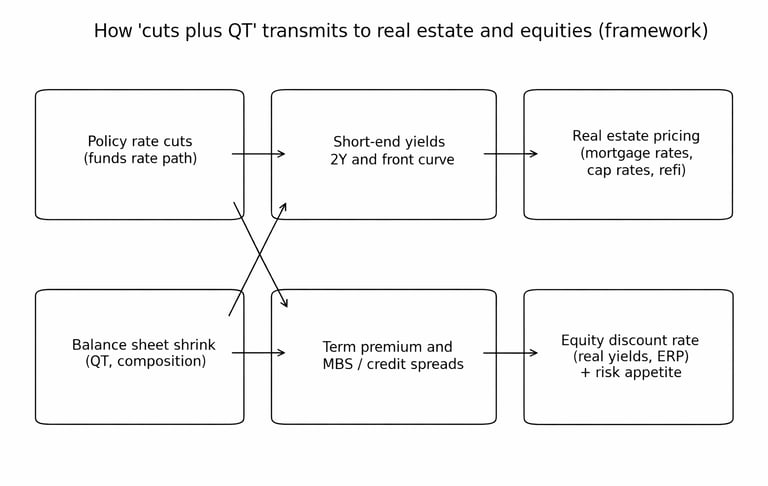

That combination matters because different levers hit different parts of the pricing stack. The funds rate and forward guidance usually move the front end quickly.

Balance-sheet policy and asset composition influence term premium, market depth, and the spread between Treasuries and mortgage-backed securities.

For housing, that spread can be as important as the level of the 10-year. For equities, term premium and real yields often dominate the discount rate.

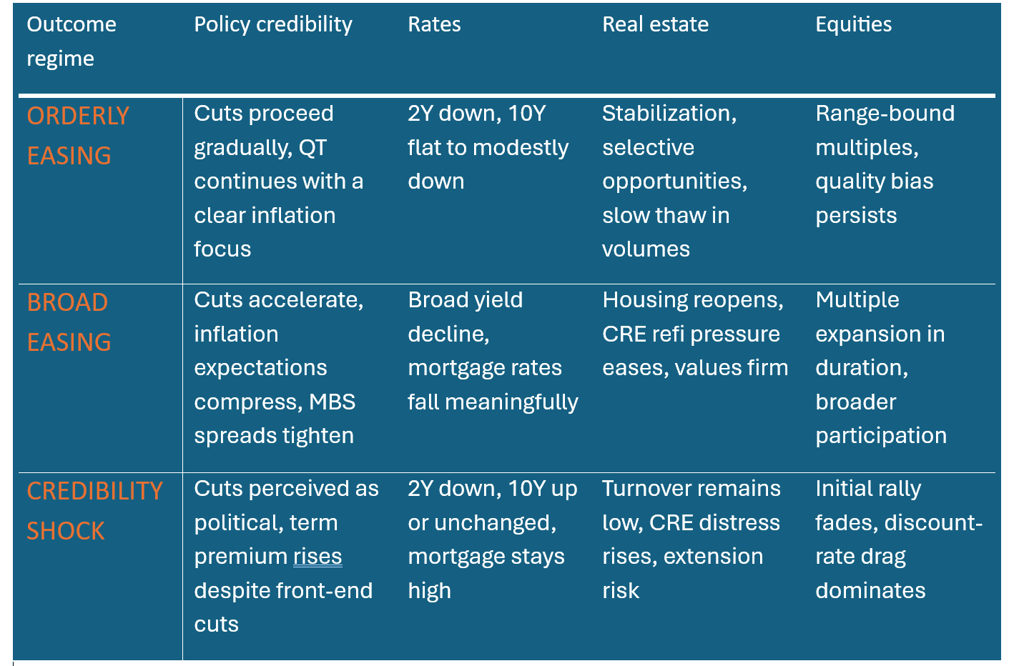

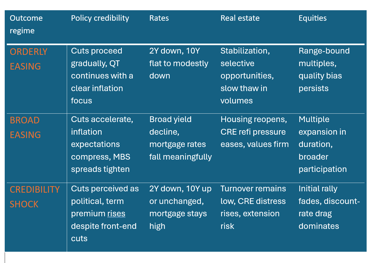

Figure 1. Transmission channels. This is a framework, not a forecast.

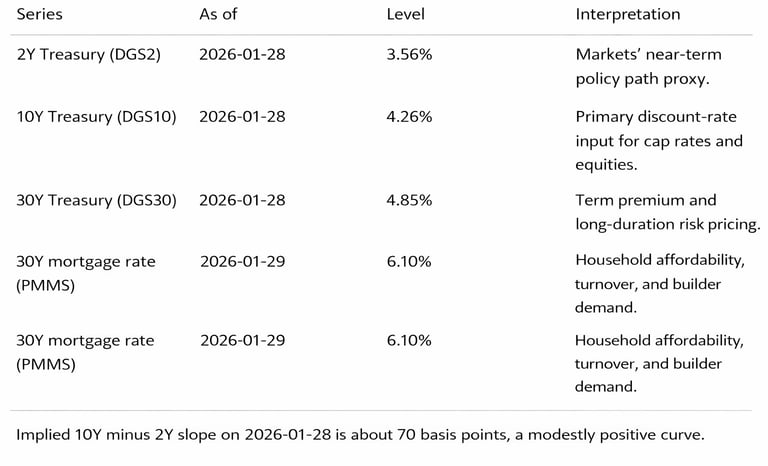

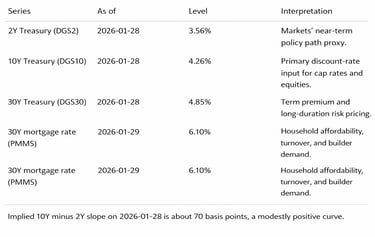

Market snapshot. The curve is already expressing skepticism

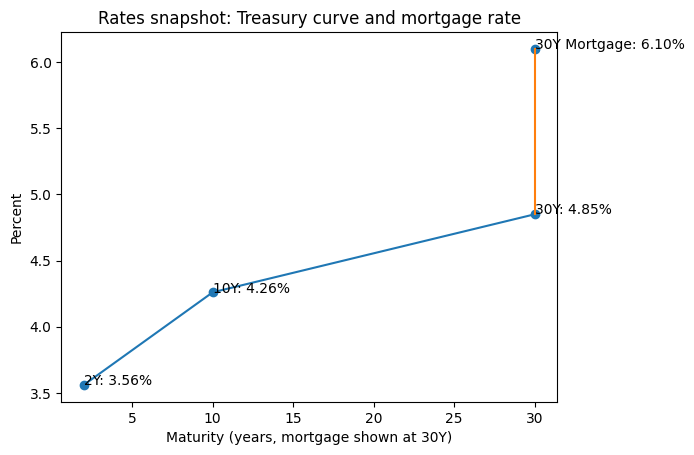

Below are reference points from Federal Reserve Economic Data series updates through January 28 to January 29, 2026. They bracket the levels cited in the interview. They also illustrate the problem. Even with a policy narrative shifting toward cuts, long rates can remain elevated if term premium, fiscal uncertainty, or inflation risk premia stay sticky.

Figure 2. Treasury curve snapshot plus mortgage rate. Sources: FRED DGS2, DGS10, DGS30 and MORTGAGE30US (Freddie Mac PMMS).

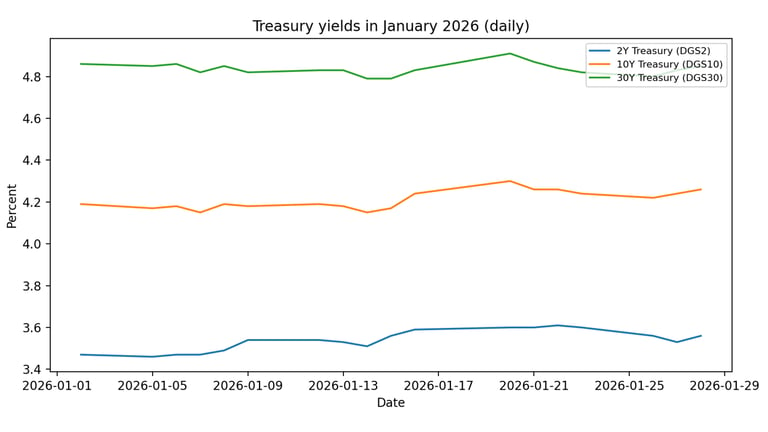

Figure 3. January 2026 Treasury yields (daily). Source: FRED DGS2, DGS10, DGS30.

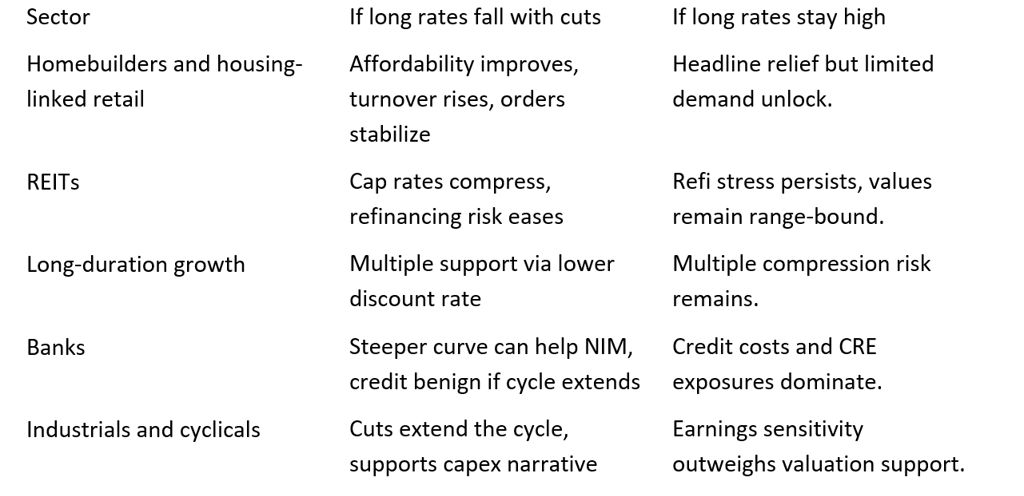

Real estate. Why the long end and MBS basis dominate

Housing and CRE react to the price of long-term money and the availability of credit, not the fed funds rate in isolation. In a cuts-plus-QT regime, three mechanical constraints can cap the upside.

Mortgage transmission. Mortgage rates are roughly the 10-year yield plus an MBS spread and lender margin. If QT or market structure keeps the MBS spread wide, mortgage rates fall less than the front end suggests.

Cap-rate math. For a stabilized asset, value approximates NOI divided by cap rate. A 50 basis point cap-rate move from 6.0% to 6.5% reduces value by about 7.7% even if NOI is flat. A move from 5.5% to 6.0% is about 9.1%. The valuation sensitivity grows as cap rates compress.

Refinancing wall and bank balance sheets. If banks maintain tight standards, transaction volume and refinancing capacity stay impaired even with lower short rates.

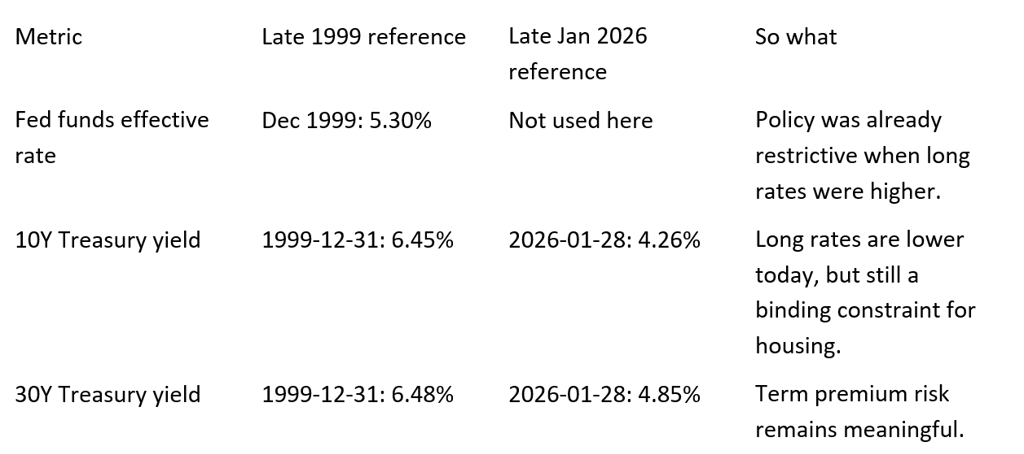

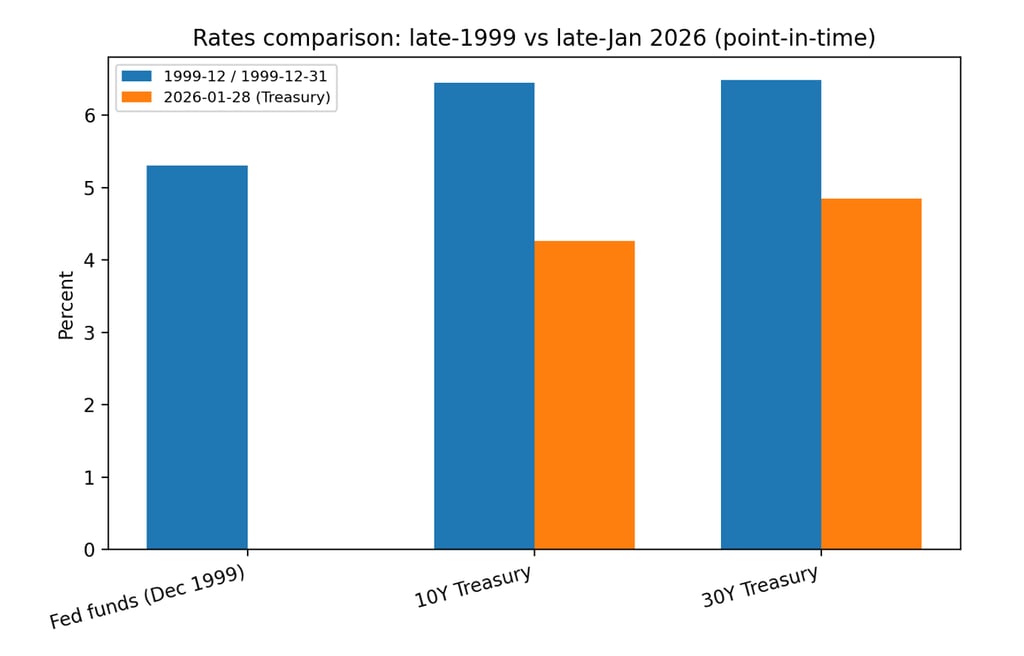

A disciplined historical anchor. Late 1999 versus today

Hassett’s late-1990s analogy is useful, but the market lesson is that strong growth plus optimism does not guarantee low long rates.

In late 1999, the 10-year and 30-year Treasury yields were in the mid-6% range while the fed funds effective rate was above 5%.

Today’s levels are lower, but still high enough that small changes have large impacts on mortgage affordability and cap rates.

Figure 4. Point-in-time rate comparison. Sources: FRED DGS10, DGS30, and FEDFUNDS.

Equities. The headline cut is not the same as lower discount rates

Equity valuation is a function of expected cash flows and the discount rate. In practice, the discount rate is a combination of the risk-free curve (often proxied by the 10-year real yield) and the equity risk premium.

Rate cuts lift equities when they reduce the discount rate without undermining earnings expectations. If cuts are interpreted as political or reactive to stress, the equity risk premium can widen and offset lower short rates.

Indicators to watch

The market will decide whether the productivity-and-fiscal narrative produces a durable easing of financial conditions. The practical test is whether the long end and spreads fall together, not whether the first cut arrives.

Indicators to watch over the next 60 to 120 days.

1. Ten-year real yield. This is the core discount-rate driver for equity duration and cap-rate pressure.

2. Mortgage rate minus the ten-year yield. If the spread widens during balance-sheet runoff, housing does not reopen even if the policy rate moves down.

3. Agency MBS spreads and dealer balance-sheet conditions. A widening basis is an early warning that QT is tightening transmission.

4. Bank credit standards and CRE refinancing availability. If standards tighten while the front end eases, distress migrates from price discovery to refinancing events.

The thesis is falsified if the ten-year declines materially while mortgage spreads stay stable or tighten, and credit spreads remain contained. In that regime, cuts transmit cleanly and both housing turnover and equity multiples can re-rate.

Primary Sources

• CNBC. “Hassett praises Trump’s pick of Warsh to lead Fed, says he has his ‘dream job’ already.” Jeff Cox. “Squawk on the Street.” January 30, 2026.

• Financial Times coverage of the Warsh nomination and market implications. January 30, 2026.

• MarketWatch live coverage citing commentary on balance-sheet size and QT considerations. January 30, 2026.

• Federal Reserve Economic Data, Federal Reserve Bank of St. Louis. Series used in charts and tables: DGS2, DGS10, DGS30, MORTGAGE30US, FEDFUNDS.

© 2025 CurveMind Inc. All rights reserved. CMI Market Intelligence is a division of CurveMind Inc.